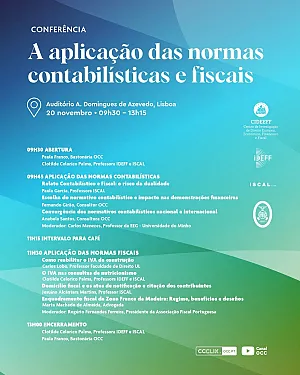

Conference "The Application of Accounting and Tax Standards"

Auditório António Domingues de Azevedo, em Lisboa | Inscrições abertas.

The Order of Chartered Accountants (OCC), in partnership with the Centre for European, Economic, Financial and Tax Law Research (CIDEEFF), the...